Is My Home in a Flood Zone?

“Is My Home in a Flood Zone? I read this article by Margaret Heidenry and I thought, wow, she has a really good point. I thought I would give you’re the summary version so you can make sure you understand flood insurance and know if you need it. A home’s risk of flooding—from hurricanes or a huge downpour—is probably not the first thing you’d think to check. However, the fact is that many U.S. homes lie within flood zones, a lot of homeowners aren’t properly aware of the risks or prepared to take them on. Most homes in high-risk flood zones are near a body of water. For instance, the Gulf Coast is one of the U.S. regions most vulnerable to hurricanes that cause flooding. Yet more than 20% of flood-related home insurance claims happen in non-flood zones, so no one should assume they’re safe. So how can you find out if your home is in a flood zone—and if it is, what protections can you put in place?

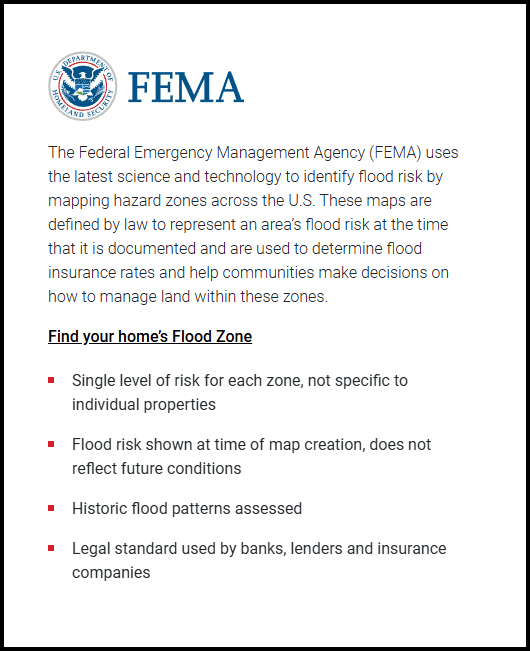

Whether you own a home or are looking to buy, here’s how to figure that out. How to find out if a home is in a flood zone There are a few ways to determine a home’s flood hazard status. One good starting point is the Realtor.com flood risk tool,(https://www.realtor.com/flood-risk/) a one-stop portal highlighting two distinct flood risk ratings for a property. The Realtor.com flood risk tool connects you directly to the Federal Emergency Management Agency site, where you can enter a property’s address and view a map showing flood zones in the area. FEMA has a little over a dozen flood zone classifications based on the estimated frequency of storms that could cause flooding in an area. The Realtor.com flood risk tool also features data from Flood Factor, created by the nonprofit First Street Foundation.

While Flood Factor works in conjunction with FEMA, this tool uses more current data based on changing climate conditions to forecast a particular home’s probability of flooding in the future. A flood risk map showing an area’s risk of flooding in the future (Flood Factor). While FEMA map sand Flood Factor ratings can certainly help you get a sense of a property’s flood risk, you should know that these numbers are only a start and are by no means a crystal ball showing you a property’s future risk of flooding with 100% certainty. Your insurance agent can also help with this. They have access to a wide range of maps and data.

Is a property’s flood zone status disclosed to home shoppers? It’s usually pretty obvious based on area and other known factors. Alaska laws about disclosing flooding, from and outside source, meaning that it wasn’t the bathtub that overflowed, it was a drainage ditch that clogged and flooded your house, or a ice dam that broke and flooded. This is required on the State of Alaska Real Property Disclosure document, but it could have flooded 2 owners ago, how would the current homeowner know? Full disclosure is certainly the ethical responsibility of the seller and the listing agent. But how can a seller know if it happened 20 years ago? This is where your insurance agent can be helpful. They may have history on the house and it’s previous problems with water. But, as a homebuyer, research the property and flood maps to see if it’s in a flood hazard area. Ask neighbors, if you’re obtaining financing, the mortgage company will also investigate the most updated flood zoning as appraisers provide that information to mortgage companies. If the property is found to be in a flood zone, the mortgage company will require flood insurance. Do you need flood insurance, plus how much does it cost? Did you know that most home insurance policies don’t cover damage or other losses caused by flooding? The federal government offers subsidized flood insurance to property owners through the National Flood Insurance Program. The average cost of flood insurance through the NFIP is around $700per year. Of course, the amount you pay will vary based on your property’s flood risk and where you are in the floodplain, as specified on the flood insurance rate map. If you are in a high flood-hazard zone, it can be significantly more expensive. Flood insurance costs will also depend on the house, including factors like years of construction, number of floors, location of the lowest floor (in relation to the base flood elevation on a flood map), building occupancy, location of contents, and your deductible.

If my home is not in a flood plain, do I need the insurance? If you live in a moderate-to low-risk area within or just outside a floodplain, should you buy flood insurance? Flood zones are based on an estimation of the number of storms that will cause flooding in a year, but there’s no guarantee that your area will flood. Still, you want to be covered in the event that something does happen. In some cases, having flood insurance is worth the peace of mind and protection it offers. *Note from Cora: Here is what I have found–insurance companies will cover damage if your tub overflows and messes up flooring, sheetrock etc., but it will no cover if a water main breaks and floods the street and then your home. Flood plain or not! If you have flood insurance, it will cover. I have seen this happen before, family was gone from the house, lots of rain that day, drainage culvert got clogged with debris, water backed up and came into the house. Family got home and their carpet was wet, and there was a mysterious mud line about 5 feet up the wall. The water was gone, but the damage was done. They were gone for only 8 hours. All sheetrock, heating system, all flooring, appliances, furniture, oh so much was just ruined. They did not have flood insurance, Why, no where near a flood plain! Literally hundreds of thousands of dollars in damage. Schnikies Batman, that’s terrible!

How to minimize your losses from flood If your home is in or near a flood zone, take these steps:

- Maintain proper grading, where the ground around your house slopes slightly downward to keep water seeping outward rather than in. In fact, a flood insurance policy typically won’t cover you if your house floods due to improper grading.

- Elevate your furnace, water heater, and electric panels to protect them from possible flood waters.• Keep storm drains and gutters free of debris, and install check valves (or one-way valves)to keep floodwater from backing into your drains.

- Seal your basement walls with waterproofing materials.

- Store your valuables and legal documents on your upper floors. Note from Cora: I have put my valuable paperwork large Ziplock bags in plastic boxes. Protected from floods–but not from fire–oh Scheesh that’s a whole other article!

Be safe! Breakup is coming, think about flood insurance. Call your insurance company. And if you want to see that house and/or buy a new one…..you know what to do! CALL ME!